Development finance institutions (DFIs) not only provide finance directly to specific projects, they also channel funds to financial intermediaries, for example local banks, in developing and emerging economies. Development banks, notably including the major multilateral development banks (MDBs) and members of the International Development Finance Club (IDFC) (together: Development Finance Institutions [DFIs]) have committed to align themselves with the Paris Agreement. While they have made (some) progress in establishing Paris lending criteria for their direct lending activities, clear rules and guidance for how to align intermediated lending with the Paris Agreement are still missing.

This blog provides a rationale for Paris alignment of DFIs’ intermediated lending and proposes a phased approach that DFIs can follow to fulfil their commitments. Even before the COVID-19 pandemic, intermediated lending represented a significant share of total commitments for many multilateral and bilateral development banks (see Figure 1). Although final data is still pending, the role of intermediated finance grew as part of the response to stabilise markets in the wake of the economic fallout from COVID-19. For example, the International Finance Corporation (IFC) committed 6 of its 8 billion USD fast-track COVID-19 support through financial intermediaries (FIs) (IFC 2020a). Experts expect intermediated lending to continue to grow.

_0.jpg) Notes: Numbers are not fully comparable among DFIs as definitions and reporting standards on FI investments are not harmonized among DFIs. For detailed information, see full report (page 8).

Notes: Numbers are not fully comparable among DFIs as definitions and reporting standards on FI investments are not harmonized among DFIs. For detailed information, see full report (page 8).

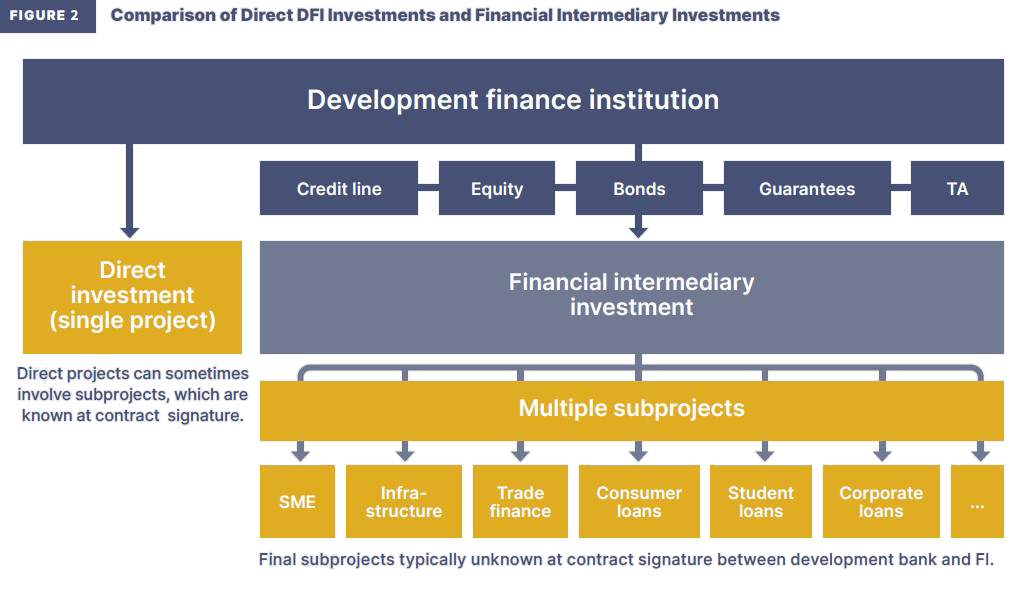

Aligning intermediated finance with the Paris Agreement is not straight forward. Local financial institutions use money provided to them to fund a variety of subprojects, the details of which are typically not yet known to the original providers of the funds at the time of their investment decision (see figure 2). This generally passes responsibility for the due diligence process and approval of the final subproject to the FI who may not have established the same lending criteria – or Paris alignment aspirations – as the development bank providing the original finance. This lending practice is a challenge that DFIs urgently need to address as finance they provide may end up supporting non-Paris-aligned investment activities.

Source: Authors.

In order to “build back better” and to honour the DFIs’ commitments to align their financial flows with the goals of the Paris Agreement (in 2017 and 2018), it is essential that the end use of intermediated finance also supports the achievement of overall climate objectives. So far, the focus of DFIs has primarily been on developing and implementing Paris aligned investment criteria for direct lending.

Some banks have started working on the issue. MDBs intend to present a joint framework for Paris alignment of intermediated finance at COP26 and the French bilateral development bank Agence Française de Développement (AFD) has established an internal working group to develop respective criteria.

How development finance institutions can align intermediated finance with global climate goals

Germanwatch, NewClimate Institute and World Resources Institute have written a working paper providing input to the discussion on how to align intermediated finance. Here are the top three things that we suggest development banks should do when considering to support a financial intermediary counterparty.

-

Develop and disclose clear Paris alignment strategies for intermediated lending with commitments for transparency and thorough oversight

1.1 A solid financial intermediary (FI) policy framework or strategy document is a key prerequisite.This should include a commitment to align intermediated finance with the Paris Agreement and set a clear timeline for when all FI investments will be Paris aligned. In many cases, this will require significant new capacity, much more transparency and more resources to oversee intermediated lending.

1.2 DFIs will need to develop the necessary capacity and organizational processes to accompany, monitor and disclose the Paris alignment assessments of final subprojects.This will mean moving away from current practice, where most DFIs dedicate significantly fewer resources to FI transactions and their subprojects than to direct lending.

1.3 It is vital to assess and disclose whether a financial intermediary meets institutional and subproject level Paris alignment standards (see also our recommendation number 2.). This would include information on where the intermediary stands in terms of capacity and organizational processes, as well as agreed steps and resources to progress. DFIs could also opt to fill capacity gaps with their own processes and help close them over time. In this case they should disclose for which time period the FI would refer projects to the development bank for Paris alignment assessments.

1.4 Paris alignment standards and requirements are meaningful to the degree that they are legally binding.Therefore, they should be included in the legal contracts with FIs.

1.5 Transparency is a prerequisite for accountability of DFIs and their financial intermediaries with regard to the implementation of standards. DFIs should thus monitor whether subprojects meet all Paris alignment criteria and disclose disaggregate subproject information. This includes addressing a crucial shortcoming of today’s practice, namely that DFIs have significantly less information about final subprojects supported by their FI clients than they have for their direct lending projects.

-

Establish robust and ambitious Paris alignment requirements for financial intermediary counterparties

For development bank investments through FI to be considered Paris aligned, FIs should meet alignment requirements in four areas: mitigation (subproject level), adaptation (subproject level), climate governance (institutional level) and transparency (institutional level).

For climate change mitigation, exclusion lists, emissions standards and transition risk assessments can help avoid high-emitting investments. To support adaptation and maximise resilience, FIs should conduct qualitative and quantitative risk assessments and integrate climate impact risk mitigation into their project design. At the institutional level, intermediaries should commit to Paris alignment and move quickly to implement this commitment by building the necessary capacity and processes. Finally, transparency and disclosure are important – and intermediaries should report on the sector breakdown of overall portfolios, provide details on subprojects financed using DFI funds, and disclose Paris alignment assessments of subprojects (see forthcoming working paper on “Aligning Financial Intermediary Investments with the Paris Agreement” for more details).

A phased approach with increasing stringency over time can ensure practicability also for FIs with limited capacity. Such an approach would define immediate requirements as well as additional steps that FIs should take over time, based on their capacity, for complete compliance. This complete process should not exceed five years.

-

Tailor the financial instrument to the climate risk of the financial intermediary counterparty

Ultimately, it is the DFIs’ responsibility to ensure that their intermediated finance is Paris aligned. To live up to this responsibility, DFIs should take a deliberate approach to selecting the investment instruments they use in FI projects, as different instruments pose varying levels of risk.

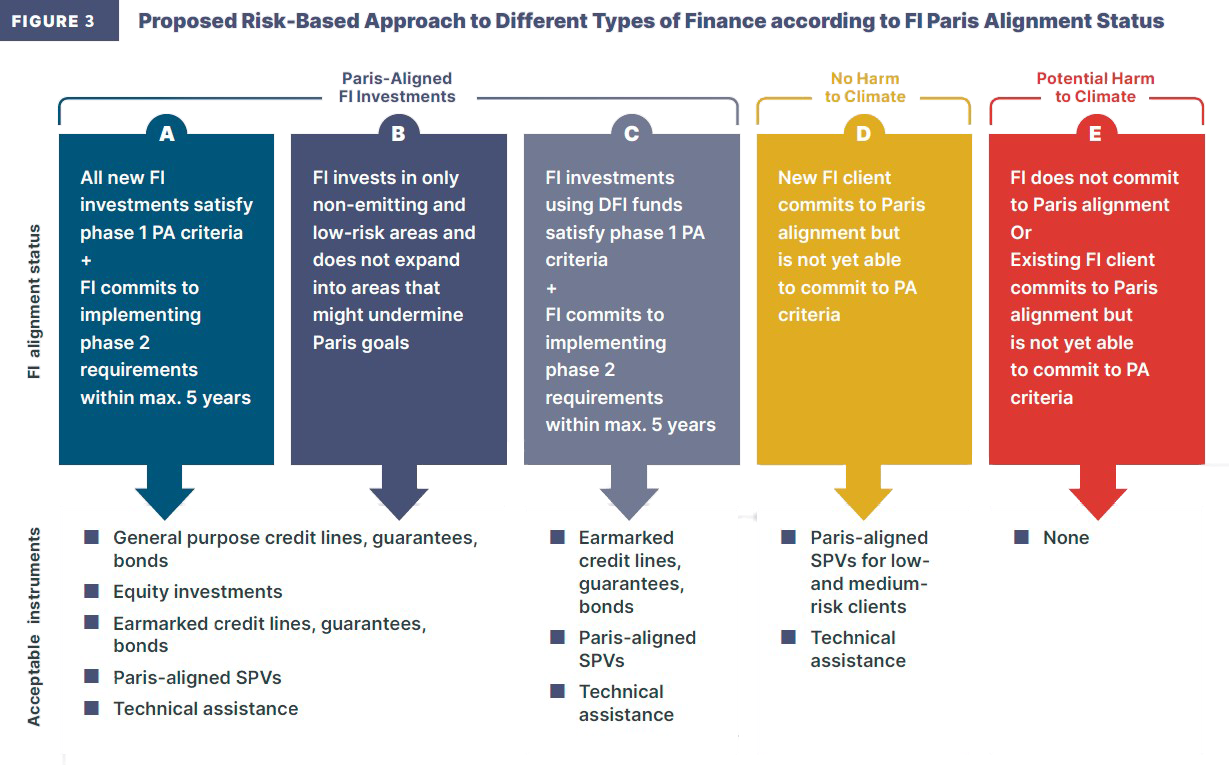

We lay out categories for DFI- investment through FIs in a Paris aligned way (Figure 3).

Source: Authors.

According to FI Paris alignment status (“Paris aligned”, “No harm to climate”, or “Risking harm to climate”), different finance instruments can be derived as acceptable.

Paris aligned financial intermediary investments (Categories A, B and C in Figure 3): General purpose lending and equity investments pose the greatest risk of supporting misaligned investments. Therefore, DFIs should only provide this kind of support to counterparties that align all their new investments – financed from DFI funds or not – with regard to mitigation, adaptation, governance, and transparency (see Category A in Figure 3) to the Paris agreement, or whose operations typically have negligible climate impacts and risk, such as small consumer loans (see Category B).

In practice, most FIs are engaged in a variety of different lending activities and often do not yet have criteria in place to screen new investments for Paris Alignment. If such an FI is generally willing to make a commitment to Paris alignment and start to implement it, DFIs could consider an engagement option. In such a case, the FI should be willing to comply with DFI Paris alignment criteria for earmarked development bank funds, commit to minimum criteria for new investments (including funds not from the DFI) and make regular progress towards complete alignment with a clear timeline that should not exceed five years. In working with these kinds of FI, DFIs will likely need to closely monitor progress, and potentially take on an important role in conducting assessments and building the capacity of FIs through technical assistance (Category C).

No harm to climate goals (Category D in Figure 3): For intermediaries that commit to the principle of Paris alignment (as 347 public development banks and 38 global private banks have already done), but who are not (yet) able to commit to implementing the criteria within the required timeline, a few options for engagement remain. These must ensure that no harm is done to climate goals and that the FI makes constant progress in aligning itself according to an agreed timeline. For example, DFIs could provide targeted technical support to new FI clients with the aim to support them in identifying climate risks or establishing a Paris alignment plan. DFIs could under certain circumstances also use a Paris-aligned special purpose vehicle.

Risking harm to climate goals (Category E in Figure 3): Financial intermediaries – existing or new – that that are not willing to commit to Paris alignment at all should not receive any (further) support.

Summary of Recommendations:

In summary, DFIs can do three things to align their financing through financial intermediaries with the goals of the Paris Agreement.

- Realize institutional changes within the DFI to support and supervise financial intermediaries more thoroughly,

- establish institutional and subproject level Paris alignment requirements for financial intermediary clients, use a phased approach and support implementation and

- select the investment instruments depending on the Paris Alignment status of the financial intermediary.

Taking these elements into account, it is of utmost importance that MDBs follow through with their announcement to present their Paris alignment approach at COP26, and for other financial institutions purporting to align themselves to also follow suit. Both MDBs and other DFIs committed to Paris alignment need to move quickly to expand their strategies and investment frameworks to include intermediated finance and set clear timetables to implement them in decision making.