Growth of Renewable Energy Sector in India

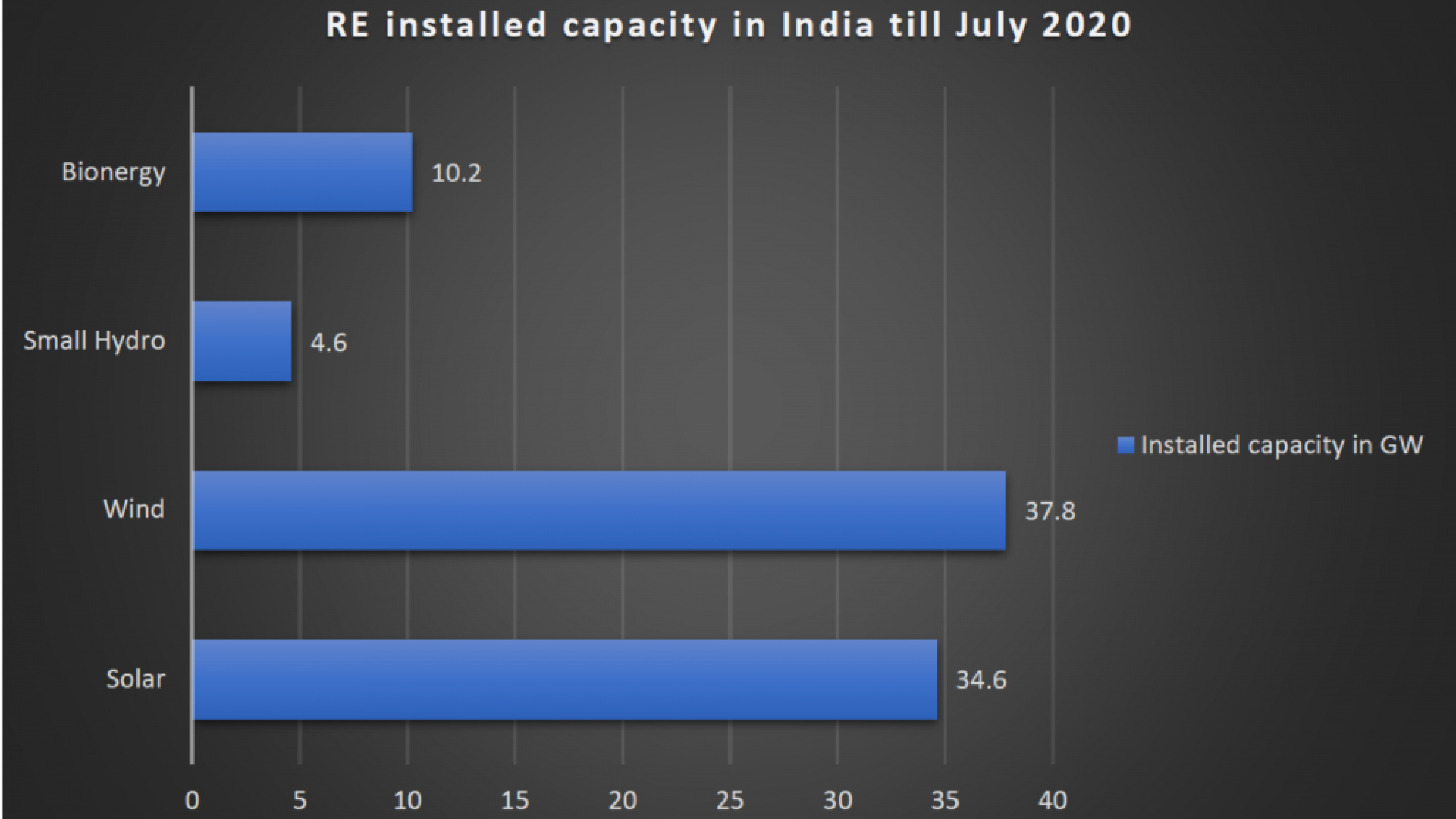

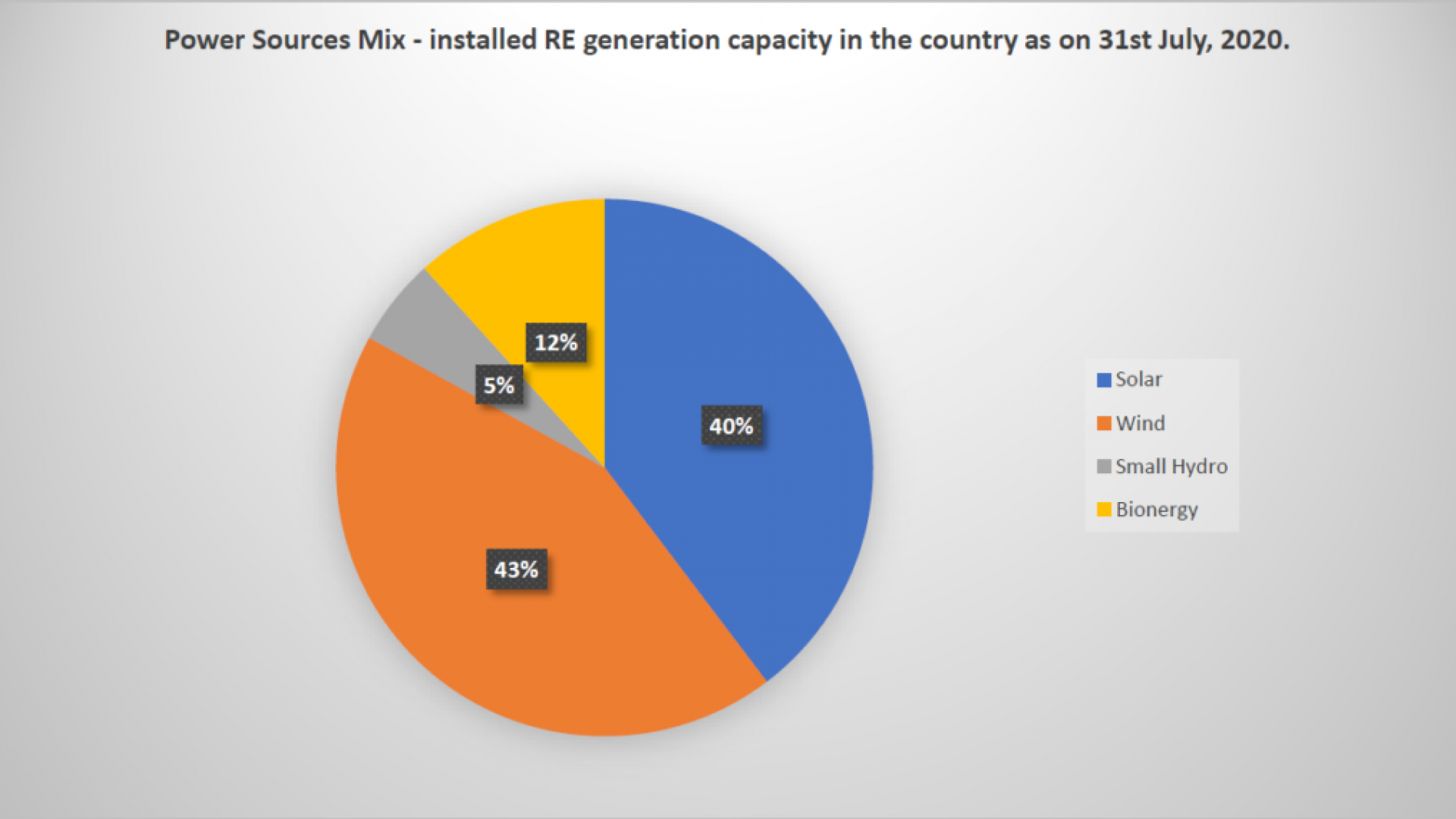

India, over the last 6 to 7 years, has witnessed significant transformations in energy systems and structures with a strong policy thrust on renewable energy (RE) and energy efficiency (EE). It has set an ambitious RE generation target of 175 GW RE installed capacity by 2022 and 450 GW of RE installed capacity by 2030. Through strong and robust policies, regulatory strategies and fiscal measures, Government of India (GoI) has been able to reach a total RE installed capacity of 88 GW by July 2020. This includes 34. 6 GW of solar, 37 GW of wind, 4.6 GW of small hydro, and 10.2 GW of Bioenergy. RE generation capacity now constitutes 23.7 percent of the total power generating capacity in the country – compared to the envisioned 40 percent of non-fossil energy generation by 2030 according to India’s NDC.

In terms of financing required, USD 38 billion will be required to meet the 175 GW target in the next 2 years, and between 2022 – 2030 approximately USD 160 billion will be required to meet the 2030 target of 450 GW. This will call for an approximate annual investment of US$ 15 – 20 billion after 2022. Many argue that this is much less than what was initially anticipated due to the declining costs of solar and wind projects. This financing requirement must be considered a conservative estimate since additional financing will be required for decentralized RE deployments (solar rooftops etc), and building transmission and storage infrastructure to integrate the generated RE effectively into the grids. Also, additional investments will be required to undertake EE measures stipulated in the various government’s policies and programmes, which are an integral part of GoI’s renewable energy programme.

EE programmes are being undertaken under the overall ambit of the Energy Conservation Act, 2001, which was enacted to reduce the emissions intensity of the economy by 33 – 35 percent by 2030 over the 2005 levels. The Bureau of Energy Efficiency (BEE) was established to implement the EC Act, and lays down regulatory guidelines for energy conservation, including the standards and labelling programme for energy efficient appliances, energy conservation codes for residential and commercial buildings, and an energy efficiency programme for energy intensive industries called Performance, Achieve and Trade (PAT). The BEE has also undertaken an ambitious programme of EE improvement and technology upgradation of five select Small and Medium Enterprise (SME) clusters in India called the “National Programme on Energy Efficiency and Technology Upgradation in SMEs”. With the increasing ownership of appliances, it is very important to ensure that the EE appliances are available in the market and are affordable. GoI’s UJALA scheme, aimed at ensuring the availability and affordability of EE lighting and fans, is an important intervention in this regard. EE initiatives have been a success but there is a dire need of private investments in EE initiatives to scale them up.

Renewable Energy Financing Landscape in India

The ambitious goals set by Government of India (GoI) have raised questions about the sources and costs of investment required to install and operate the renewable energy infrastructure. Unlike the conventional power generation capacity, which is largely under the direct ownership of Central and state governments, the renewable energy sector is driven by commercial private interests. Financing for the renewable energy sector in India comes from the private investors and corporates (which provide the equity investments required for the sector), and the national and international commercial banks, non – banking Financial Companies (NBFCs), institutional investors, and development banks (which provide the requisite debt financing for the RE projects).

Financing in India is one of the most significant challenges to the expansion of renewable energy infrastructure. Issues such as the non–availability of low–cost, long tenure debt, shallow bond market, and the reluctance of the banking sector and institutional investors to lend to the RE and EE projects due to perceived risks and regulatory restrictions have prevented financing from reaching the renewable energy sector at the scale and pace required to meet India’s renewable energy targets. Several Independent Power Producers (IPPs) are now planning to offer initial public offering, opening the market for broader investor participation. Green Bonds issued by banks and Non-Banking Financial Companies (NBFCs) is also likely to become an important source of debt for the future.

The Indian Government through a number of robust policies, regulatory and fiscal measures, and direct financial support encourages private investment in the renewable energy sector. These measures help assuage the risk perception of investors and encourage them to invest in the RE sector. Direct financial support from the government is extended through government agencies such as IREDA, Power Finance Corporation (PFC) and Rural Electrification Corporation (REC), which gives financial support to the RE sector in the form of soft loans, counter–guarantees, and securitization of future cash flows. Funds are sourced from the National Clean Energy and Environment Fund (NCEEF), and international banks and development agencies such as European Investment Bank (EIB), World Bank, Japan International Cooperation Agency (JICA) and KfW.

Interventions to support the financing of the Indian systemic energy transition in the aftermath of the Corona Pandemic

As long-term economic recovery in the aftermath of the pandemic is planned, the Indian Government must extend and continue to support policy and fiscal interventions aimed at de-risking investments in the renewable energy sector. In this context, international financial institutions can play an important role in extending financial support to renewable energy sector in India, especially during the Covid recovery. Finance flowing from bilateral and multilateral development agencies and banks, can help free up government money to be deployed in the RE and EE projects to catalyse private investment in the sector.

Additionally, low-interest, long-term loans can be extended by agencies such as German KfW, Japanese JICA, the Dutch FMO and Austrian OEEB for the RE and EE sector. These can be routed through government agencies such as the Indian Renewable Energy Development Agency (IREDA), the Power Finance Corporation (PFC), and the Rural Electrification Corporation (REC). While this is already happening to some extent, it needs to be significantly scaled up to enable RE and EE based green recovery in India. Donor money can also be invested in the form of private equity in the RE, DRE and EE projects, and can be deployed as financial guarantees, credit – enhancement support and payment – security instruments. In all these forms, international finance can catalyse private investment in the renewable energy sector in India significantly. Indo-German cooperation can play an important role in this regard. The German Government can (1) support GoI’s investment de–risking measures by providing financial support for it, (2) invest in renewable energy projects by collaborating with German investors interested in investing in such projects in India, (3) partially cover risks of the investors keen to invest in Indian renewable energy market, and (4) provide low-cost concessional loans to the renewable energy investors in India via the Indian NBFCs and Banks. It can also through technological cooperation provide support to GoI efforts in modernizing grids, and provide support for collaborative research and development in the RE, DRE and EE technologies. Indo–German Energy Forum is an important platform in this regard. It brings together stakeholders, ranging from policy makers, businesses, and think tanks giving opportunity to brainstorm on ideas on RE, DRE, EE, grid integration, raising finances, and collaborative R& D.

Apart from direct financial support, “international finance institutions can help build strategy and support policy development; convene relevant stakeholders and decision makers across the public and private sectors; and through these activities greatly enhance what the private sector can do” (Petersburg Climate Dialogue, 2020). International Solar Alliance (ISA) – with Germany possibly joining in soon - can also play an important role in this regard by cooperating with other bilateral and multilateral development agencies and funds to help RE and EE producers in India get access to affordable debt.

This blog post first appeared on 12/16/2020 on the website of our partner, the Vasudha Foundation and is part of a joint blog post series on Green and Resilient Recovery in India:

Read the other blog posts on this topic:

- Green Recovery in India to Strengthen Sustainable Agriculture

- Promotion of Renewable Energy at the heart of Green Recovery in India

- Green Recovery in India to Strengthen Overall Social Resilience

- Principles and Criteria of Green Recovery in India that enable NDC-enhancement in 2021